Report

The Arctic Zone of the Russian Federation: development prospects and risks

April 2024

The Arctic Zone of the Russian Federation: development prospects and risks

200 mtpa – total volume of cargo generated by mining projects that have been jeopardized by sanctions and severance of business ties.

Mining projects generating more than 200 mtpa1 of cargo, as well as the Northern Sea Route (NSR), a national transportation artery of vital strategic, economic, and political importance, are at risk.

Meanwhile, the race for the Arctic is on. In recent years, more and more states have been revisiting their Arctic strategies, ramping up investment and activities there, rightly seeing the Arctic as a macro-region of major strategic importance.

The strategic importance of the region is underpinned by its wealth of valuable minerals, the marine routes that run through it, and the military presence of major world powers.

According to various estimates, the Arctic is home to 25–30% of the world's undiscovered oil and gas reserves, as well as wealthy deposits of precious metals, such as palladium and platinum. The development of the Arctic region and concurrent development of attendant infrastructure allows to slash the time required to transport goods between Europe and Asia. For instance, the length of the route along the NSR is 40% shorter than the traditional transportation corridor through the Suez Canal. Other competitive advantages of this corridor include the absence of strict limitations on vessel size and zero risks of pirate attacks compared to the unsafe Gulf of Aden and the South China Sea. These days shipping companies tend to circumvent Africa. Besides, flight time between North America and the Middle East is 20% shorter compared to nonpolar routes.

The importance of the Arctic has been fully realized by many leading states, which in recent years have stepped up efforts to develop the mineral resources of these territories, for example, through investments and joint ventures. Yet in other areas confrontation is growing.

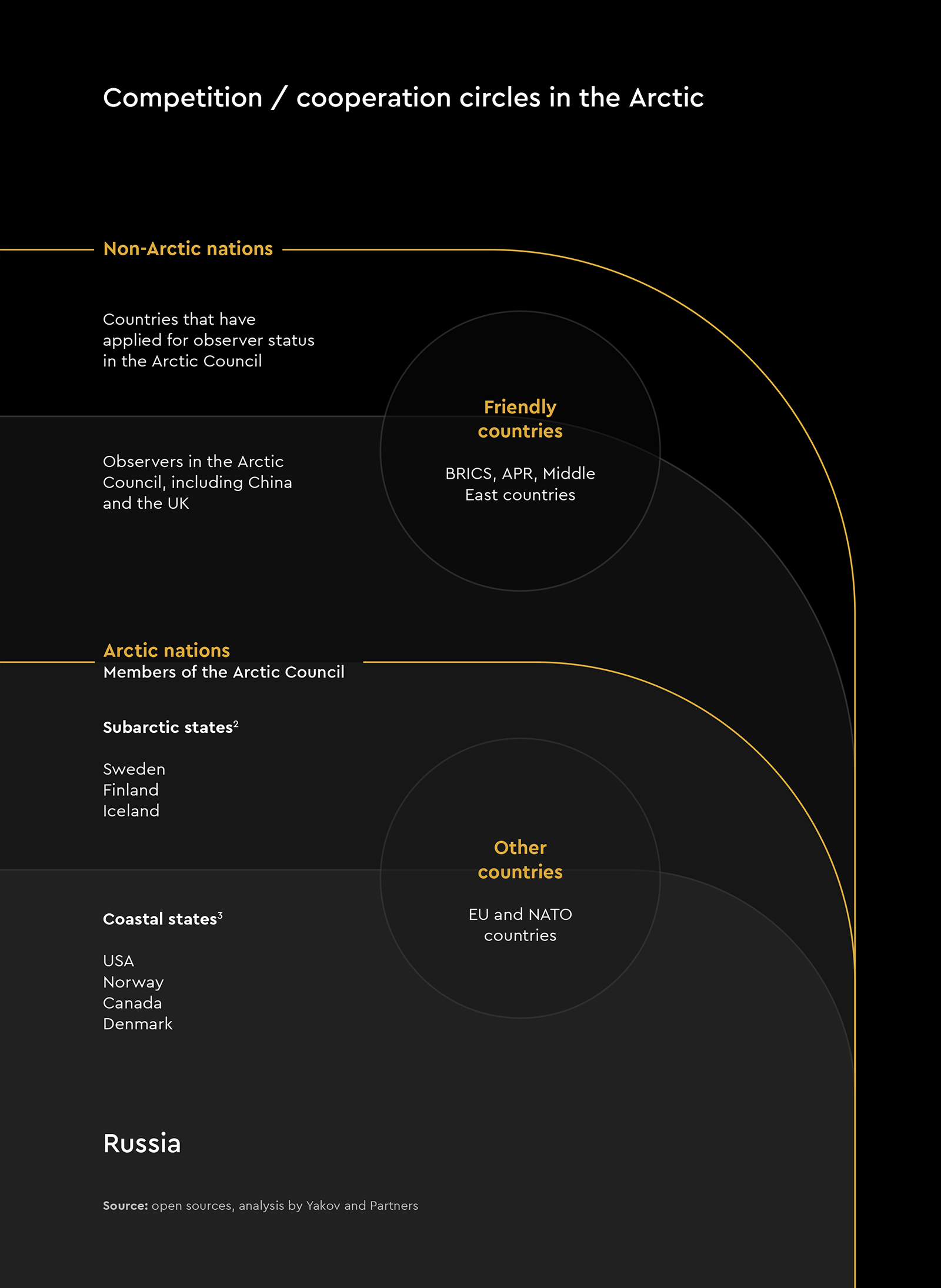

According to our estimates, increasing geopolitical rivalry and global warming will spur the race for the Arctic in the next 20 years. In addition to the Arctic coastal states, other countries are also showing a growing interest in the region. The most striking examples are China, which calls itself "near-Arctic", and the United Kingdom, "the Arctic's nearest neighbor". In our opinion, their first steps towards development of Arctic territories will be to legitimize their activities in the Arctic.

It is important to keep in mind that there is no separate document that would fully define the legal status of the Arctic. The UN Convention on the Law of the Sea [UNCLOS] adopted in 1982 is the main legal framework for international maritime law defining the legal status of ocean spaces and resources, including the interaction related to maritime activities among subjects of international law. Yet it fails to regulate many aspects of such activities, especially with regard to the continental shelf, which is subject to a special legal regime. Coastal states enjoy exclusive sovereign rights over the continental shelf, including the right to explore and exploit the natural resources. Taking advantage of the special status of the shelf, Arctic nations have historically resorted to delimiting the shelf and making territorial claims against one another. One such example would be the territorial dispute between the United States and Canada over the Beaufort Sea which is thought to contain significant oil and natural gas reserves, including undiscovered fields.

As for the Russian Arctic shelf, the most heated discussion of the past 20 years unfolded around the Lomonosov Ridge, the rights to which are also claimed by Canada and Denmark. According to the estimates, this shelf area boasts some of the richest hydrocarbon reserves. The Russian Ministry of Natural Resources estimated the total volume of oil and gas resources in the zone of the Central Arctic submarine elevations complex at up to 5 billion tonnes of oil equivalent.

In 2023, the Commission on the Limits of the Continental Shelf (CLCS) approved Russia's claims to seabed rights for 1.7 million square kilometers in the central Arctic Ocean. Since then, the Russian Federation has submitted a revised claim for part of the Amundsen Basin and might put in a submission for the Gakkel Ridge.

At the same time, it is highly probable that similar applications by Canada and Denmark will also be approved by the CLCS in the future. In this case, the countries will have to bilaterally negotiate the delineation of the shelf in accordance with the UNCLOS procedures. It should be noted that Canada has also ratified UNCLOS, which means that it has de jure and de facto abandoned the sectoral approach.

The increasing geopolitical rivalry in the region is also evidenced by the events of 2022–2024. For example, in the fall of 2022, the US Department of Defense established a special unit that would handle emerging issues in the region and expects to complete an update of its current Arctic strategy in the near future.

In June 2023, the Nordic Defence Cooperation (NORDEFCO, a collaboration among the five Nordic countries) and NATO allies held Arctic Challenge Exercise, a massive war games exercise involving 150 fighter jets and 3,000 soldiers. The US has been consistently escalating the tensions to this day. For example, in February, over 8,000 soldiers took part in an international military exercise hosted by the US in Alaska to adapt to the extreme weather conditions of the Arctic. Undoubtedly, this ramp-up of the military presence is aimed at sustaining the US influence in the region.

In turn, in December 2023, Russia orbited its Arktika-M hydrometeorological satellite No. 2 designed to monitor climate and environment in the Arctic region and secure uninterrupted satellite connections. Four more Arktika satellites are to be built and launched by 2031. The new satellites will be used primarily for reliable communications along the NSR.

Given the increased focus of various militaries and the economic potential of the region, the Arctic may well turn into a new hotbed of geopolitical risks.

Since the beginning of 2022, Russia's participation in key bodies and platforms for international cooperation on Arctic development has been limited as the Arctic Council nations discontinued their cooperation with Russia, while the Barents/Euro-Arctic Council (BEAC) refused to transfer the presidency to Russia, prompting the latter to withdraw from the Council.

However, dialog with our Western partners continues on other platforms, albeit less influential ones. In particular, Russia maintains its membership in the Arctic Economic Council (the last meeting was held on the margins of the Eastern Economic Forum in Vladivostok in September 2022), participates in the Northern Forum, the International Arctic Science Committee (IASC), the International Arctic Social Sciences Association (IASSA), and the International Union for Circumpolar Health (IUCH).

Russia’s priorities in the Arctic outlined in the Russian Foreign Policy Concept include establishing mutually beneficial cooperation with non-Arctic states that pursue a constructive policy towards Russia and are interested in international activities in the region. Therefore, the Russian Federation will be able to initiate interaction on a bilateral basis with Asian countries, as well as within BRICS, while recognizing the role of the Arctic Council as the leading platform for international dialog.

Fierce competition stimulates Russia to invest heavily in the development of its northern territories and exploration of mineral resources in the Arctic.

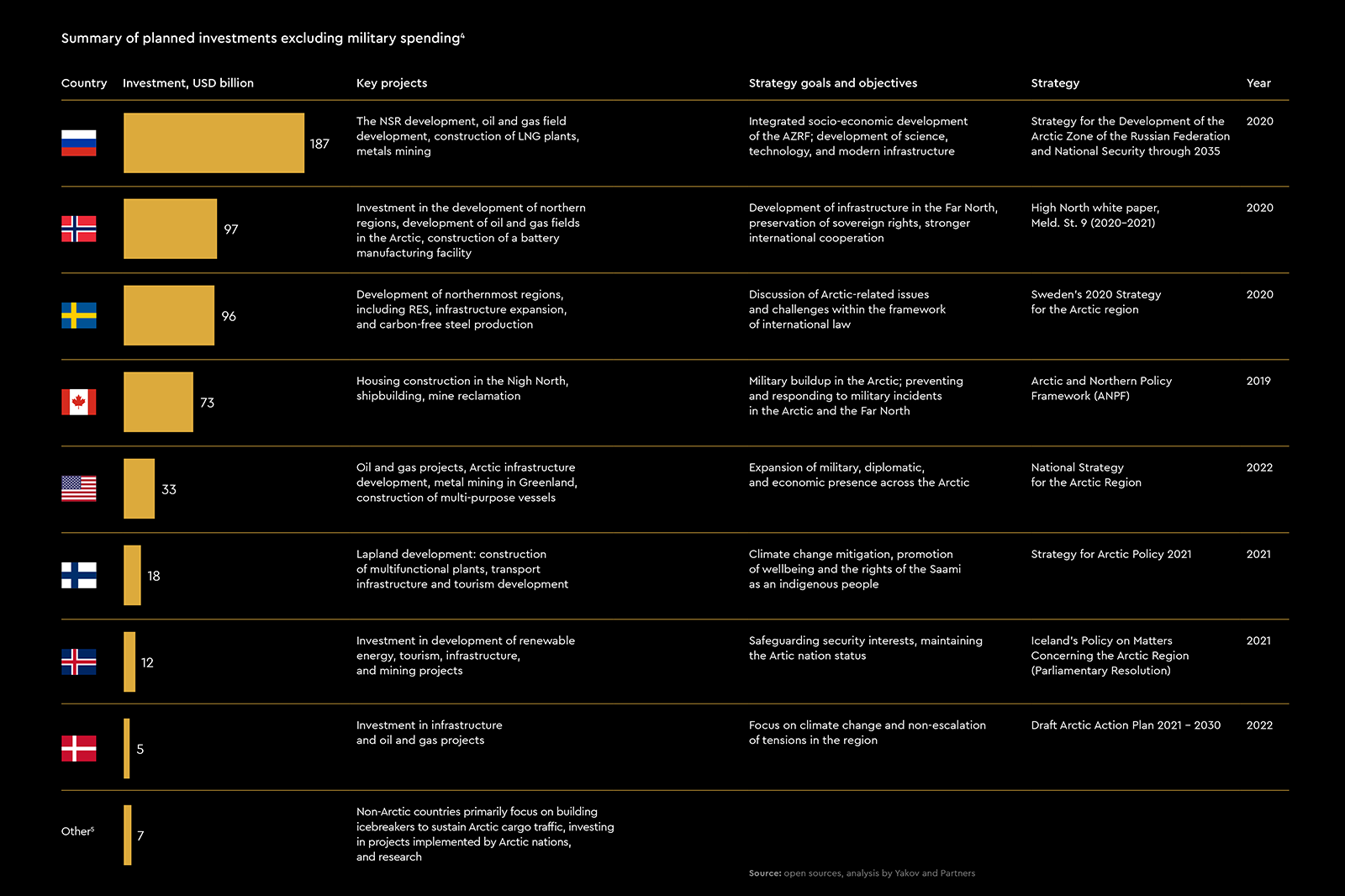

187 bn USD – the amount of investments contemplated in the AZRF Development strategy through 2035

According to the Arctic Zone Development Strategy 2035, Russia plans to invest USD 187 billion into the region development, beating its closest competitors, Norway and Sweden, by a large margin. The investment will go towards expanding the NSR, developing oil and gas fields, mining metals and coal, building LNG plants, as well as solving social problems, i. e. improving the quality of life of the indigenous population and social conditions of economic activity.

We believe Russia will have to straddle the line between cultivating partnerships with other states and maintaining control over the Arctic territories and the NSR when implementing its strategic projects.

This means Russia will be faced with two challenges:

- Sustaining trade relations, carrying out joint investment projects in the Arctic, joint scientific research, and technology exchange while maintaining full control and without creating any leverage for foreign influence.

- Keeping full national control over the NSR and setting the rules for its use (including navigation, icebreaker support, navigation safety, and environmental protection) while consistently ramping up international transit traffic.

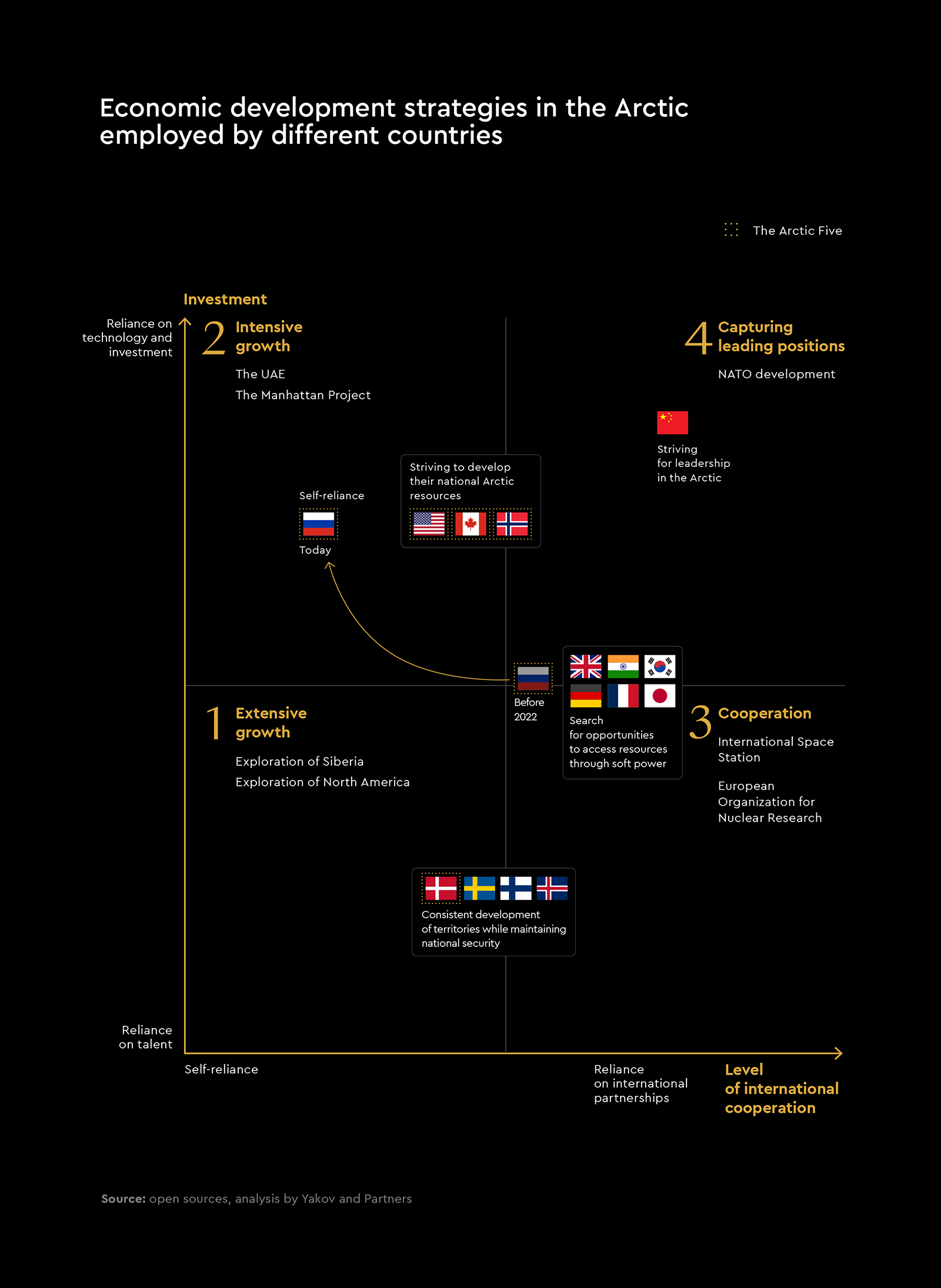

Different countries employ different economic development strategies in the Arctic, depending on the available investment resources and readiness for international cooperation. Although until February 2022 Russia leaned towards full-scale international cooperation, not least in the scientific realm, it now has to rely on its own resources.

Norway relies on sustainable and innovative development of the Arctic, aligning the pace of development of the northern and southern regions of the country, and bolstering military cooperation with NATO and with other Nordic countries to maintain security in the region. All NATO countries in the North prioritize the Northeast Atlantic with its sea routes. Norway tends to actively participate in the policy of "containment" of Russia in the Far North, which fits into the overall NATO strategy.

It also needs to increase hydrocarbon production in the Barents Sea to maintain its status as a key energy supplier to the EU and pushes for deep-sea mining of "green" metals. The country aims to implement major infrastructure projects and develop high-tech industries in the region (Arctic 2030 program).

Strategic goals and interests in the Arctic

- Deter the "Russian aggression" alongside its borders.

- Ensure a military presence and boost coast guard capabilities.

- Strengthen its leadership in the Arctic Council in 2023–2025.

- Strengthen its sovereignty over Svalbard.

Short-term goals

- The key short-term goals include increasing the defense capabilities and protecting energy assets.

Sweden is primarily interested in increasing the EU and NATO influence in the Arctic. Its core motivation is to strengthen the collective power of the allies to ensure security and research development.

Strategic goals and interests in the Arctic

- Build up its Arctic profile, strengthen the agreement with NATO members to develop and improve joint deterrence and defense capabilities.

- Bolster defense cooperation with the Nordic countries.

Short-term goals

- Increase military spending on the Arctic.

- Invest in building energy infrastructure.

Denmark seeks to reinforce the defense ties with the Nordic countries and the United States without escalating towards total militarization. The governments of Greenland, the Faroe Islands, and Denmark are currently working on a new Arctic strategy through 2030. Denmark leans towards an alliance with the US, as Greenland is home to US military and research bases. The country claims the right to the Lomonosov Ridge near the North Pole, which extends about 1,800 kilometers from the Novosibirsk Islands to Ellesmere Island and which is also challenged by Russia and Canada.

Strategic goals and interests in the Arctic

- Minimize tensions in its relations with Greenland, retain sovereignty over Greenland (98% of the territory) in order to maintain the status of an Arctic power.

- Restrain the growth of US influence in terms of anti-Russian and anti-Chinese policy in the Arctic.

- Develop mining projects to buoy economic growth.

Short-term goals

- Develop security cooperation with neighboring Arctic nations.

- Invest in ramping up military capabilities in the Arctic.

The US views the Arctic through the lens of competition of superpowers, recognizing the increased military and economic presence of Russia and China and considering it a major security challenge in the region.

The 2022 US National Strategy for the Arctic Region envisages an increased military, diplomatic, and economic presence in the region, as well as continued investment to deter Russia and China in the region and to support sustainable development aimed at improving the quality of life of Alaska and Arctic indigenous peoples.

In December 2023, the US State Department released a new Extended Continental Shelf map covering an area of about 1 million square kilometers, mostly in the Arctic and the Bering Sea (territories that are also claimed by Canada and are close to Russia's borders).

By extending the shelf area, the US obviously seeks to access more areas rich in critical minerals needed to produce batteries for electric cars, as well as more oil and gas deposits. At the same time, the US is yet to ratify the UN Convention on the Law of the Sea, so its claims to expand its part of the continental shelf in the Arctic are currently devoid of any international legal basis.

Strategic goals and interests in the Arctic

- Establish Arctic domination (commercially, diplomatically, and scientifically).

- Develop oil and gas resources.

- Break the monopoly of the Russian merchant and naval fleet.

- Secure a platform for launching ballistic missiles.

Short-term goals

- Short-term objectives in the region focus on improving the quality of Arctic bases and training their military forces in the extreme conditions of the Arctic.

Given Canada's focus on the adverse effects climate change has on the northern part of the country, its 2019 Arctic and Northern Policy Framework includes conservation of biodiversity, protecting and restoring ecosystems, and protecting the interests of indigenous peoples. In addition, the updated framework takes into account potential challenges stemming from the increasing activities of other countries in the region. It should also be noted that Canada’s boundary dispute with the US over the Beaufort Sea, which is thought to contain rich oil and gas deposits, has remained unresolved since 2006.

Strategic goals and interests in the Arctic

- Expand infrastructure in the northern part of the country to maintain the sovereignty and security of the Arctic and the North.

- Solve climate problems caused by melting ice.

- Develop natural resources.

Short-term goals

- Develop Arctic infrastructure.

- Invest into resource development.

Through a combination of investment and commercial activities, research and humanitarian projects, participation in regional development, and initiatives in Arctic governance, China is progressively strengthening its geopolitical role in the region without confronting the Arctic nations. However, China's self-proclaimed status as a "near-Arctic state" is underpinned by an increase in its activity in the region.

Strategic goals and interests in the Arctic

- Participate in the development of mineral resources, especially hydrocarbons.

- Cut the length of major transportation routes.

Short-term goals

- Develop the alternative Transpolar Sea Route (TSR, the Polar Silk Road) and/or make the NSR part of the Belt and Road Initiative.

- Ramp up naval operations in the Far North and the Arctic.

Calling itself the Arctic's "nearest neighbor", the UK sees its legitimate interests in respect to environmental, security, and prosperity issues in the region. It will seek to position itself as the leading non-regional military power in the Arctic, thus securing its economic interests.

Strategic goals and interests in the Arctic

- Gain influence in the region, build up military presence.

- Ensure the freedom of navigation and access to Arctic waters.

- Secure the status as a leading supplier of hydrographic, meteorological, and oceanographic data on the Arctic to NATO.

Short-term goals

- Work on climate change issues.

- Stimulate international cooperation.

While Arctic nations tend to focus on national security issues, attaching particular importance to defensive measures and military buildup in the region to safeguard their Arctic borders, other states pay more attention to non-military aspects and seek to maximize the economic benefits of their Arctic presence without losing sight of the need to curb increasing confrontation and strengthen international cooperation in the region.

60% of Arctic hydrocarbon reserves are located in the regions owned or claimed by Russia

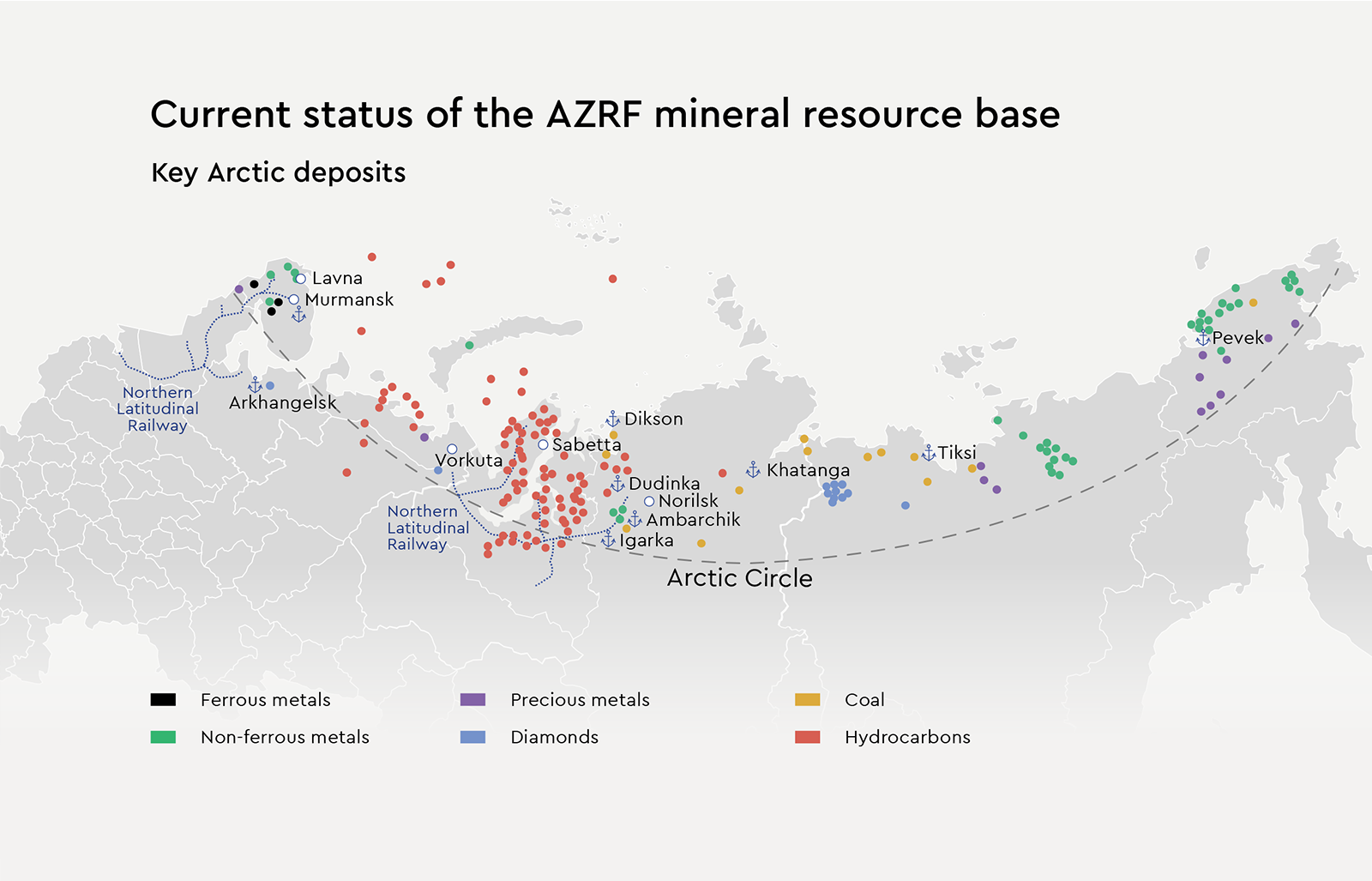

The Arctic territories span 4.8 million square kilometers, or 28% of the country's total territory, and are home to 2.6 million people. The AZRF boasts huge mineral deposits, including hydrocarbon fields. According to various estimates, more than 60% of the Arctic’s hydrocarbon reserves, or about 250 billion barrels of oil equivalent (BOE), and 35% (more than 9.5 billion tonnes) of solid minerals are located in the regions owned or claimed by Russia.

Mining is especially developed in the North of Russia. Siberia has rich reserves of almost all known precious metals: gold, silver, nickel, molybdenum, and zinc. There are also huge deposits of coal and diamonds in the region. The Republic of Sakha (Yakutia) accounts for about a quarter of global diamond production. The Russian North supplies copper, iron, tin, platinum, palladium, apatites, titanium, rare earth metals (REM), and many more valuable minerals. A substantial part of ferrous and non-ferrous metal reserves is located on the Kola Peninsula.

The AZRF development is an important factor that opens up new opportunities for economic growth in the country. As already mentioned, the key document that outlines long-term plans for the region is the Strategy for the Development of the Arctic Zone of the Russian Federation and National Security through 2035, adopted in 2020.

The main strategy objectives in order of priority

- Maintain sovereignty and the conflict-free zone status through fostering diplomatic cooperation.

- Ensure rational use of natural resources for sustainable economic development in the region and nation-wide.

- Stimulate social development to improve the quality of life, healthcare, education, and economic opportunities for the residents, including indigenous peoples of the North.

41 vessels make up the Russian icebreaking fleet, including seven nuclear-powered icebreakers: the three commissioned Project 22220 vessels, the Taimyr, the Vaigach, the Yamal, and the 50 Let Pobedy.

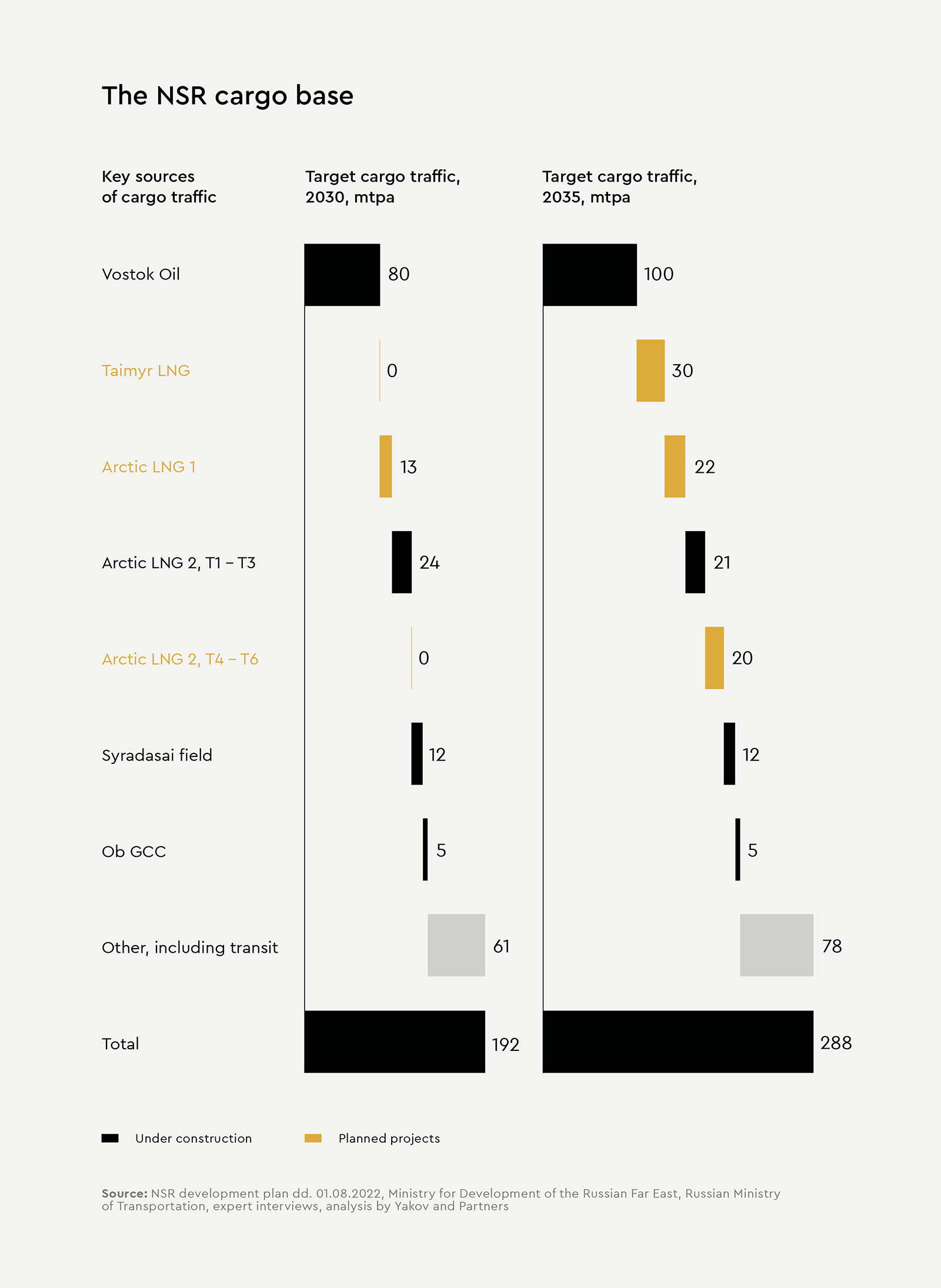

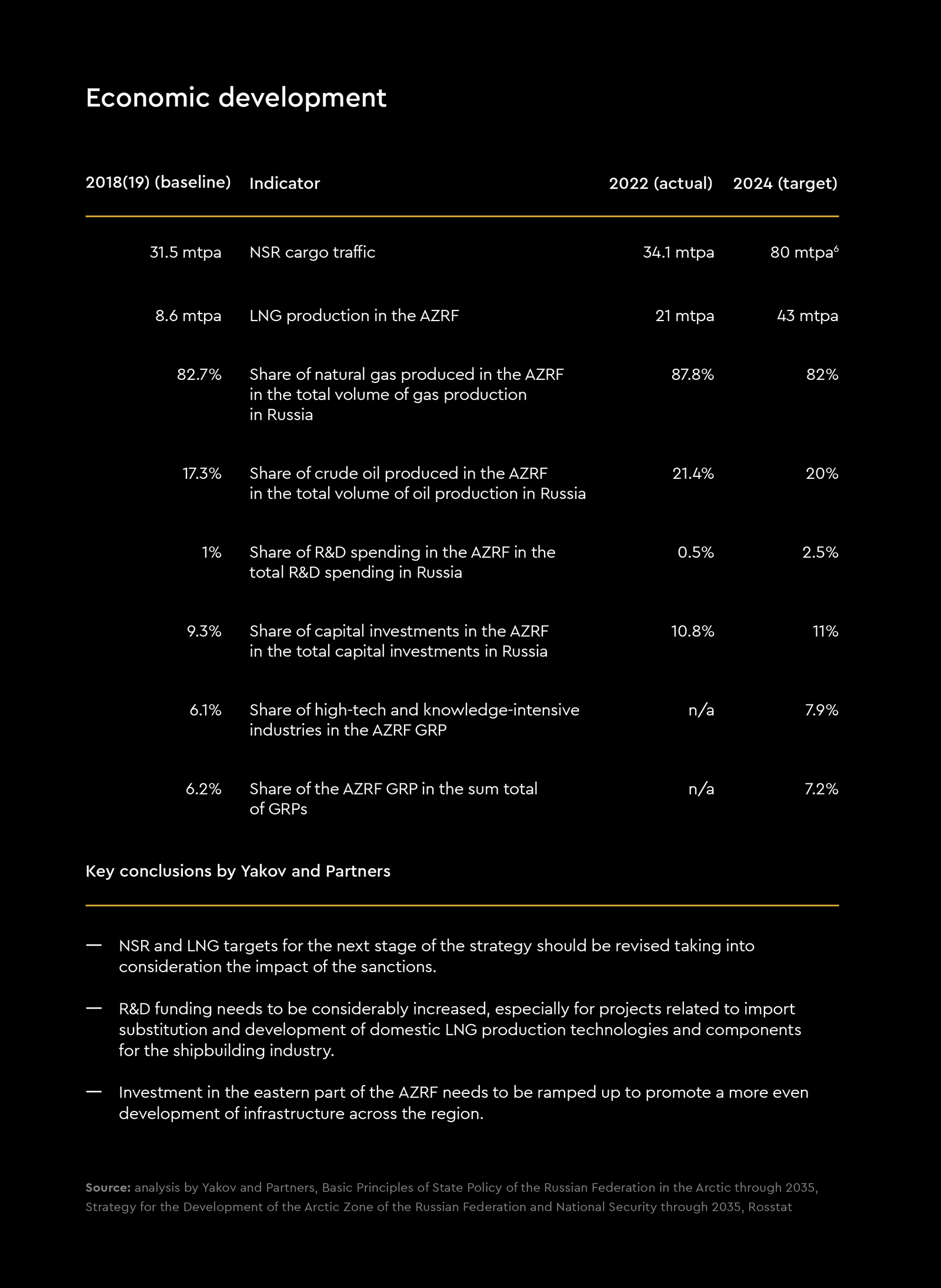

The Arctic strategy envisages a 3.4 p. p. rise in the share of the AZRF GRP in the total GRP of Russian regions by 2035 (vs the 2019 baseline), at least a 99 mtpa increase in the volume of transportation along the NSR, and at least a 82 mtpa boost in LNG production by 2035. The implementation of the Arctic development plan is expected to have a positive impact on the social sphere, adding 200,000 new jobs and helping bring down unemployment by 0.2 pp. In 2022, a separate NSR development plan until 2035 was approved, according to which cargo traffic targets should increase to 220 mtpa.

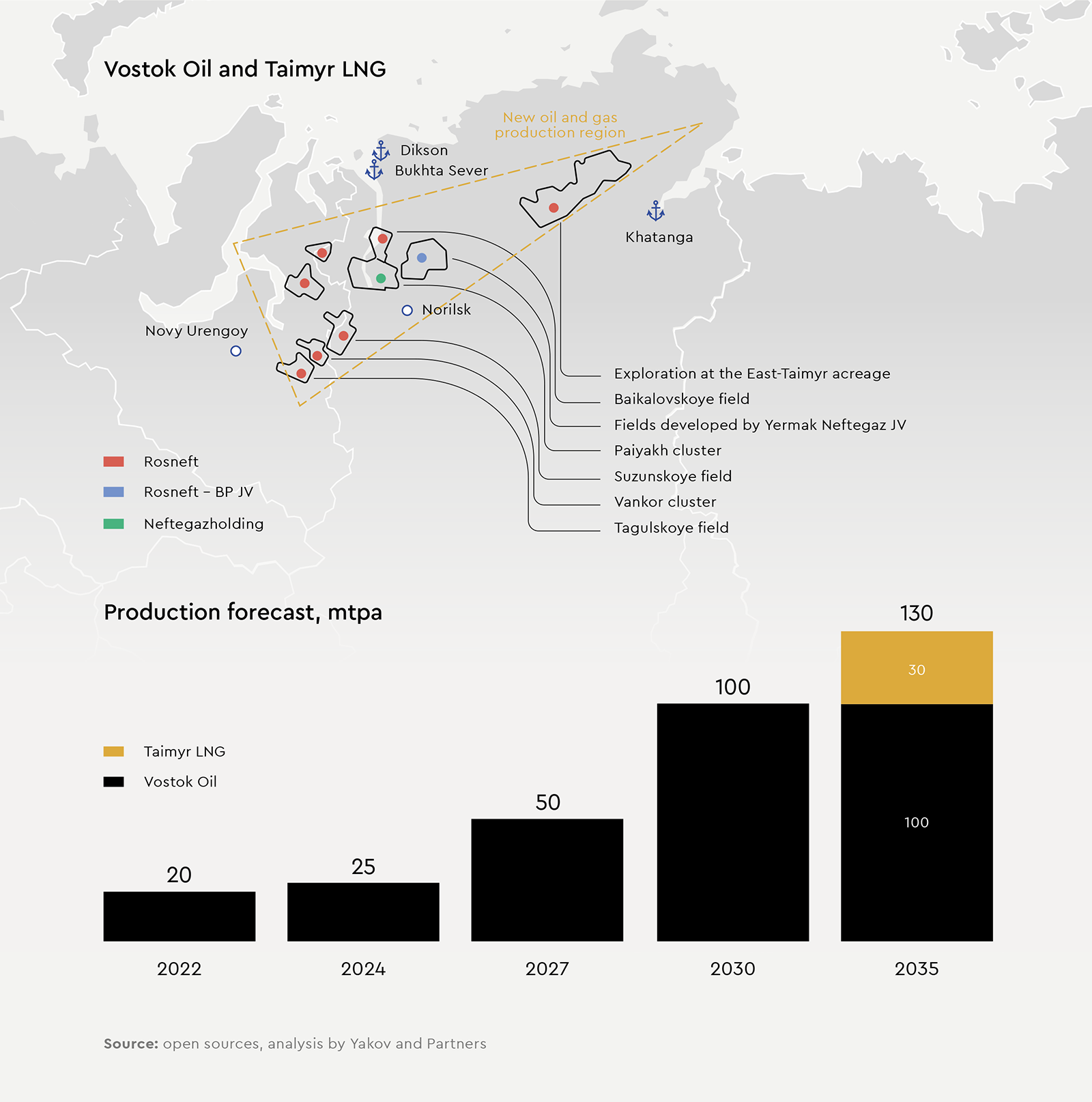

Major investment projects in the Arctic are primarily aimed at hydrocarbon production: Vostok Oil and the associated Taimyr LNG, as well as Arctic LNG 1, Arctic LNG 2, and the Ob LNG project. Plans to develop the Syradasai deposit, one of the world's largest coal deposits, are also in the works.

Vostok Oil, the largest oil development project in Russia, is being implemented by Rosneft. The total reserves of light low-sulfur oil on the Taimyr Peninsula amount to 5 billion tonnes, and by 2030 annual production is expected to reach 100 mtpa. The success of this endeavor will determine the fate of yet another ambitious project, Taimyr LNG, which is set to be implemented on Vostok Oil's resource base. The gas liquefaction plant with a capacity of 35–50 mtpa will be located at Bukhta Sever in Krasnoyarsk Krai and is expected to be launched in 2030–2035. The announced investment amount is RUB 12 trillion.

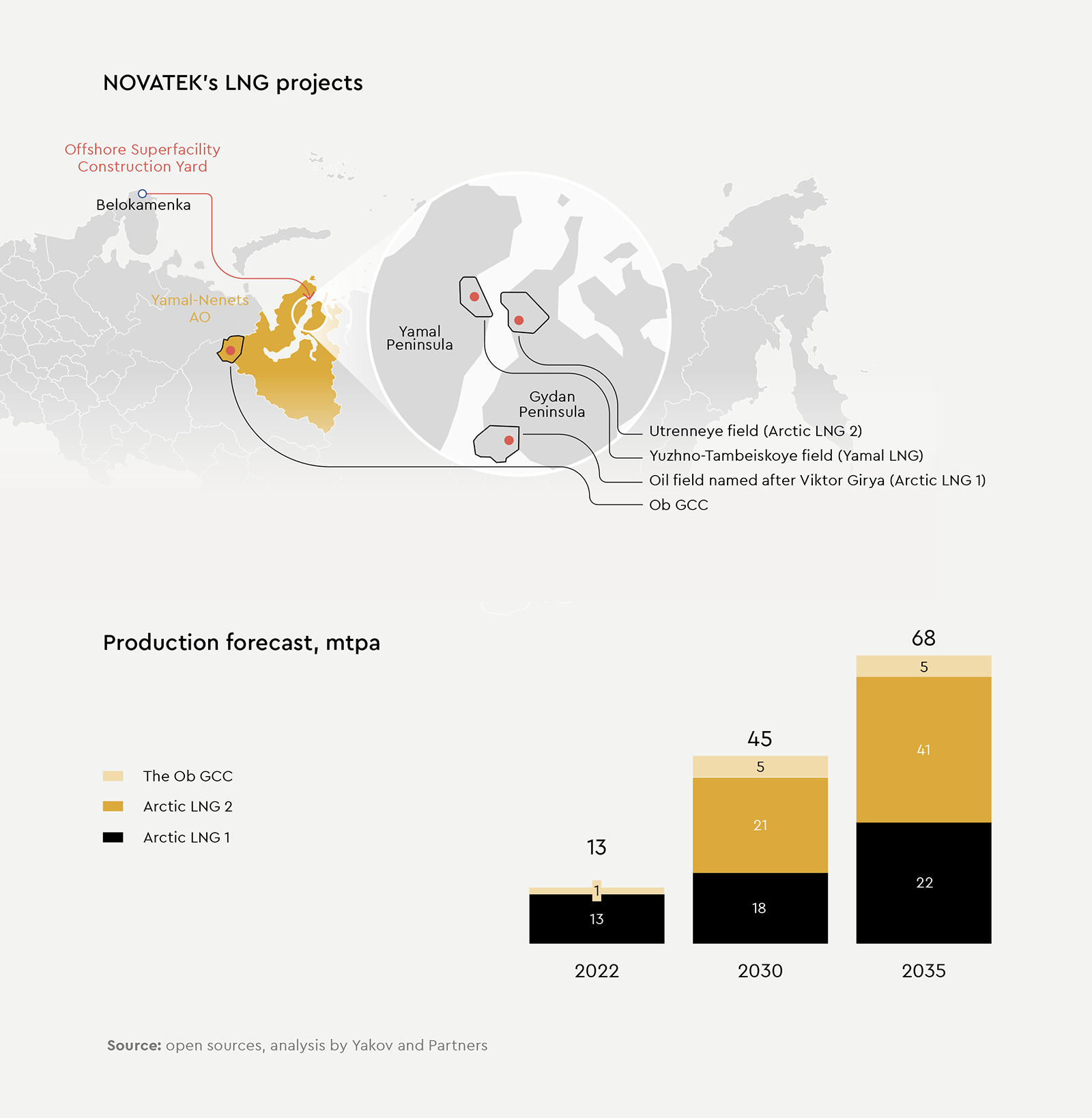

Another large-scale project, NOVATEK's Arctic LNG 2 on the Gydan Peninsula, is already underway. Its first stage includes building three process trains with a total capacity of 21.4 mtpa; the launch is planned for 2023–2026.The second stage of Arctic LNG 2 involves the construction of three more process trains with a total capacity of 19.8 mtpa (to be launched after 2030).

Two other NOVATEK projects have been put on ice. In September 2022, the company postponed the construction of the Ob Gas Chemical Complex (GCC). The facility was expected to produce up to 2.2 mtpa of ammonia and 130,000 tonnes of hydrogen per year. The project also included construction of two 3-mtpa LNG process trains. The fate of yet another project, the Arctic LNG 1 plant with a design capacity of 20 mtpa, will be determined after the decision regarding the Ob GCC has been made.

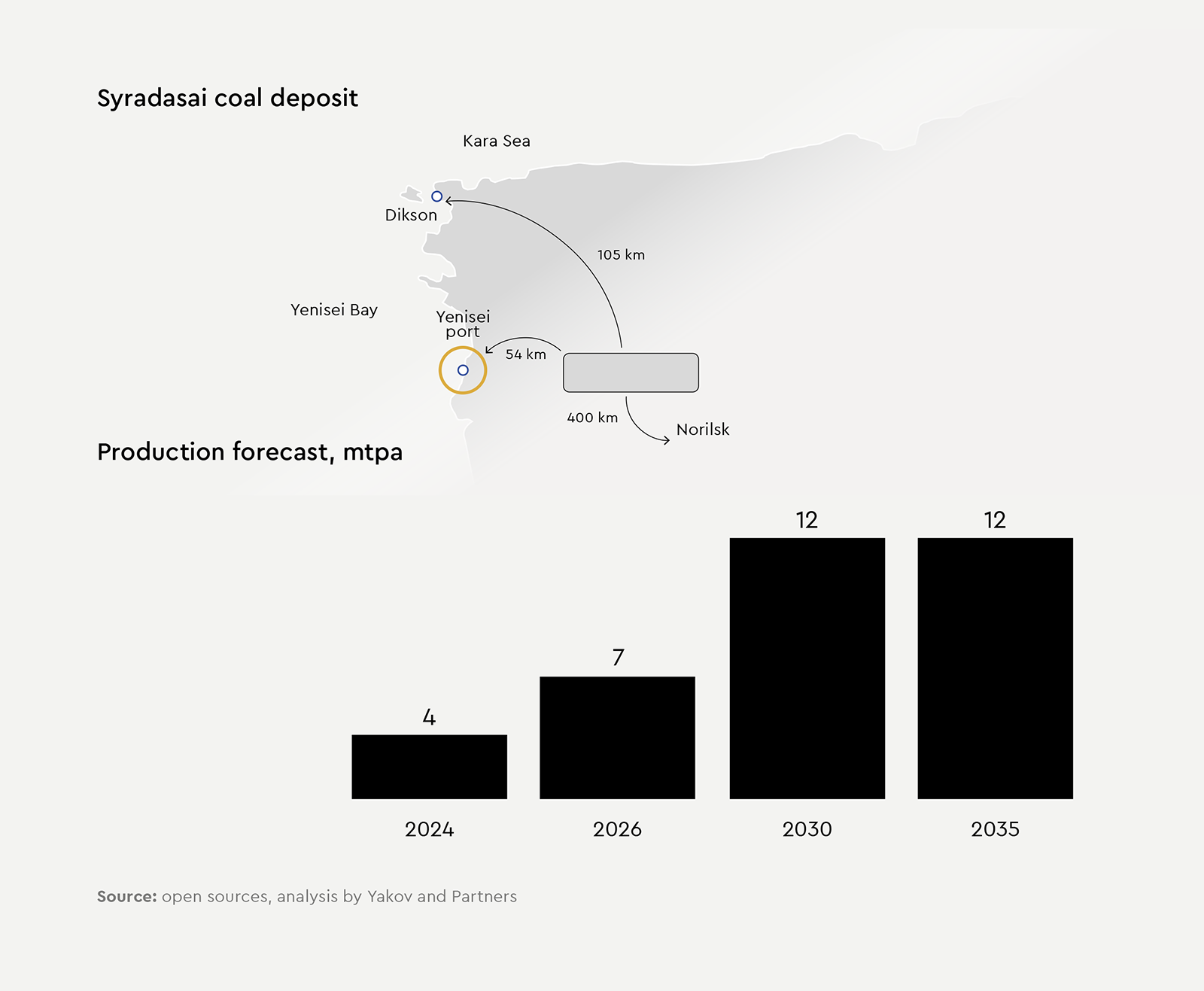

In addition to oil and gas projects, the Syradasai field is being developed in Taimyr, with resources estimated at more than 5 billion tonnes of hard coal of various grades. Severnaya Zvezda (part of AEON Holding) plans to invest more than RUB 45 billion into the project by 2025, with total investment estimated at RUB 100 billion.

At the first stage, the mining and processing plant will produce up to 5 mtpa of coal concentrate, and following the commissioning of the second process line in 2029, the capacity will increase to 12 mtpa. The project also includes the construction of the Yenisei seaport whose cargo turnover is expected to reach 10 mtpa in 3-4 years.

In total, these Arctic projects are expected to provide an additional 200 mtpa of cargo shipped via the NSR by 2035. The announced volume of investment exceeds RUB 15 trillion (USD 170 billion); another RUB 1.8 trillion (USD 20 billion) is to be invested in the NSR infrastructure development.

According to Rosatom's data, more than 36 mtpa of cargo traveled via the NSR in 2023. If the optimistic NSR development scenario prepared by the Ministry for the Development of the Russian Far East is realized, the volume of transportation may grow to 288 mtpa by 2035, with more than 70% of the traffic coming from the seven large-scale mining projects.

Establishing year-round navigation along the NSR requires innovative icebreakers with increased icebreaking capability and speed. At present, three Project 22220 multi-purpose nuclear-powered icebreakers are on duty in the NSR area – the flagship icebreaker the Arctic and the serial icebreakers the Siberia and the Ural. These icebreakers are evidence of the superior technological level of the Russian industry, which is capable of producing unique vessels operating in the harshest weather conditions of the Arctic.

FSUE Atomflot (part of Rosatom) has commissioned the construction of several more Project 22220 nuclear icebreakers. The Yakutia and the Chukotka are already being built at the Baltic Shipyard owned by the United Shipbuilding Corporation (contractual delivery dates are December 2024 and December 2026, respectively). At the end of January this year, the keel-laying ceremony for the fifth serial ship, the Leningrad, was held; the ceremony for the sixth ship, the Stalingrad, is scheduled for the next year. Rosatom also intends to have a series of four diesel icebreakers built; the flagship vessel is to be delivered in 2028.

Several of the Project Leader vessels, the world’s most powerful nuclear-powered icebreakers (propulsion power of 120 MW) capable of breaking 4 to 5-meter-thick ice, are to be commissioned at the Zvezda shipyard by 2032.

Today Russia's icebreaker fleet consists of 41 vessels, including seven nuclear-powered icebreakers: the three commissioned Project 22220 vessels, the Taimyr, the Vaigach, the Yamal, and the 50 Let Pobedy.

The brand-new nuclear-powered vessels complete with high-tech equipment will propel the Russian icebreaker fleet to a whole new level and accelerate the NSR development.

Market access risks

In November 2023, the US announced sanctions targeting Arctic LNG 2, forcing the investor to find new contractors and technologies and engage Turkish equipment suppliers. Later that year foreign shareholders TotalEnergies (France), CNPC and CNOOC (China), and the Mitsui / JOGMEC consortium (Japan) declared force majeure on their participation in the project. Later, the UK joined in on the sanctions.

The first stage of the Arctic LNG 2 project has already been launched, and the first lots of liquefied natural gas are ready for export. At the same time, the Chinese and Japanese companies are considering to seek exemptions from the US sanctions on Russian LNG. Until this issue is resolved, the facility will have to sell gas on the spot market.

The situation calls for exploring options to increase economically viable shipments to Asia-Pacific (APR) countries, as well as to Turkey, India, Pakistan, and other friendly countries. NOVATEK has already taken steps in this direction: in February 2023, the Russian company and India's DFPCL signed a MoU on the supply of LNG and low-carbon ammonia.

The demand for LNG on the global energy market will continue to grow in the medium term, which means Russia may establish itself as a market leader if Arctic LNG 2 volumes are successfully redirected.

Lack of ice-class fleet

Despite the high pace of icebreaker construction, all seven key Arctic projects are faced with the challenge of securing enough large super ice-class vessels (tankers, gas carriers, bulk carriers). Under the optimistic scenario, these projects are expected to produce 210 mtpa of hydrocarbons by 2035.

According to our estimates, this will require about 200 ice-class vessels, primarily tankers and gas carriers, to ensure the export of products. Among the existing shipyards in Russia, only SSC Zvezda could take on production of such vessels, but its capacity alone is insufficient to fully meet the demand for fleet. On top of that, the Russian Government banned foreign-made vessels from shipping coal via the NSR starting from March 2026 (Decree No. 1964 dd. 02.11.2022).

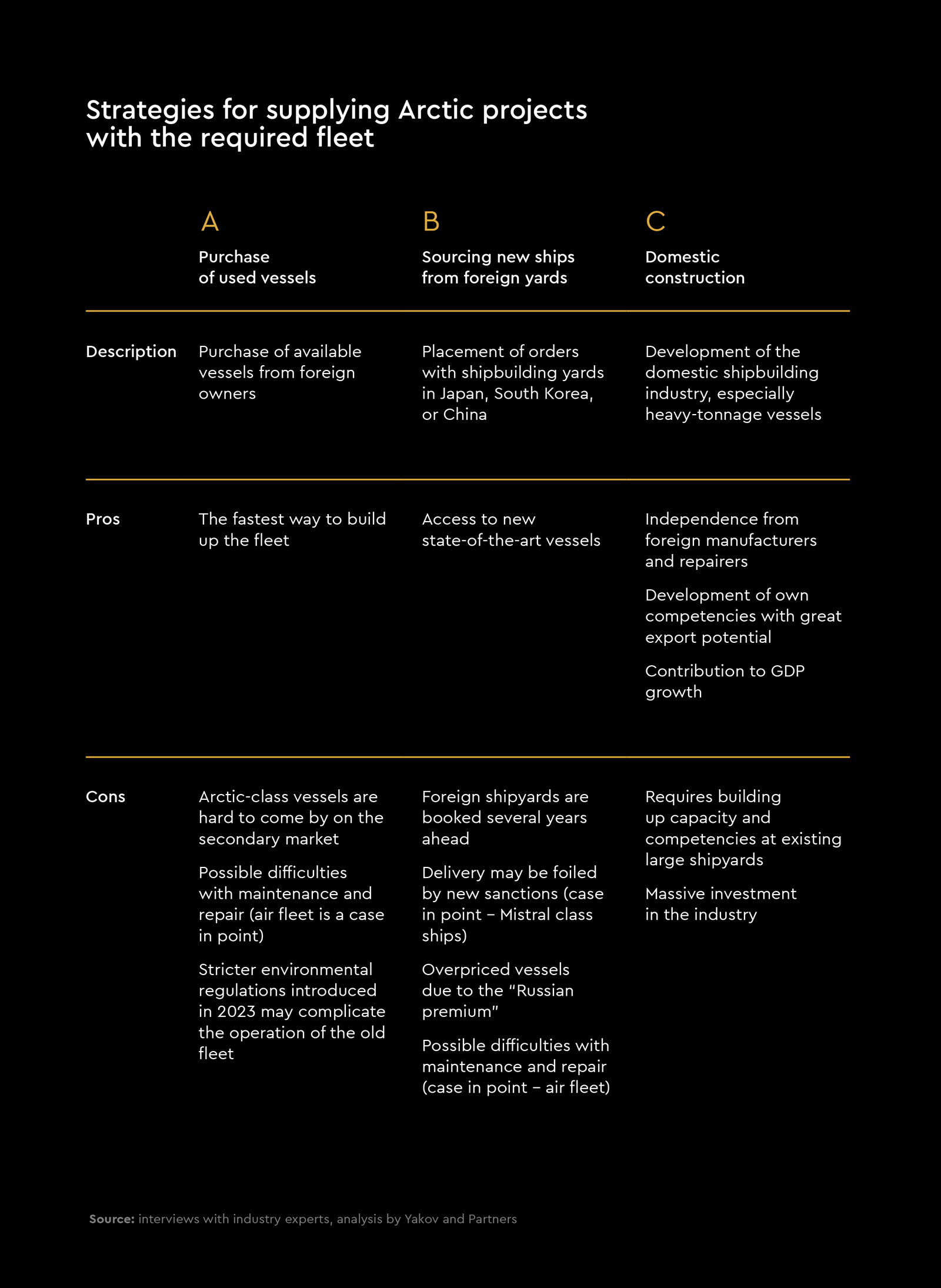

We see three possible options for supplying new Arctic projects with the ice-class transportation fleet they require:

- purchase and lease of second-hand vessels previously operated in Arctic conditions;

- ordering new vessels from foreign shipyards;

- domestic construction

А Purchase and lease Sourcing new ships from foreign yards

This option is the least viable, as there are no eligible vessels owned by companies from friendly countries on the market today.

According to our calculations, only 24 out of 748 LNG carriers meet the necessary criteria, with 22 vessels being operated by Russian companies, one vessel by a US-based company, and another one by a Norway-based company. Of the 2,319 oil tankers currently in operation around the world, only nine meet the necessary criteria; two of them are being operated by Russian companies and the other seven are being operated by Greek companies.

The practice of raid transshipment, when cargoes are reloaded from Arctic-class vessels to ordinary ones, may help improve fleet availability. For example, it was revealed in December that NOVATEK resumed board-to-board transshipment of LNG in the Kilda Strait. The company also has the access to floating LNG storage facilities in the Murmansk Region and Kamchatka Krai. However, it should be kept in mind that this approach only partially solves logistical problems which will only exacerbate as hydrocarbon export volumes grow.

В Sourcing new ships from foreign yards

Speaking of foreign opportunities, it should be taken into account that vessels of the required ice class could be commissioned to shipyards in just three countries – South Korea, China, and Japan. Yet South Korean and Chinese shipyards are currently booked until 2028–2029. It is also necessary to take into account the time and cost of such construction, as well as the risk of non-fulfillment of orders (for example, new tankers and bulk carriers will cost about twice as much as used vessels). Besides, under the pressure of sanctions, some foreign shipyards building the largest numbers of tankers and dry bulk carriers may turn down Russian orders, which has happened before. For example, South Korea’s DSME canceled the contract for the construction of three gas carriers for Arctic LNG 2 in 2022. And even if orders are successfully fulfilled (for instance, in China), the price of new vessels will include the so-called Russian risk premium.

С Domestic construction of ice-class vessels

In the absence of available vessels on the market or an opportunity to place orders abroad, Russia needs to focus on domestic shipbuilding. Given the circumstances, this is the only attractive and reliable option which also holds long-term prospects – but first Russian shipbuilders will have to overcome several major challenges.

The main problem stems from insufficient capacity at large shipyards, as well as the need to find domestic substitutes for machinery and industrial components. While small and medium shipyards in Russia are unable to handle orders for large vessels, large yards are either fully booked with orders for non-target vessels (like the Offshore Superfacility Construction Yard near the village of Belokamenka, Murmansk Region, which is currently handling orders from NOVATEK) or lack large-block assembly capabilities. At the same time, investments in setting up efficient large-block ship assembly are comparable to the construction of a new shipyard.

Ramping up the capacity of SSC Zvezda would be one way of solving the problem. However, it is difficult to say now whether this option is commercially viable.

Judging by the experience of China and South Korea, development of the shipbuilding industry may take 10 to 15 years providing the government takes the lead in this process. Among the specific foreign practices that could help accelerate shipbuilding development in this country, the following should be emphasized:

- massive state support to help industry players upgrade and develop infrastructure and shipyards and speed up shipbuilding;

- support for projects aimed at import substitution, production of machinery components and construction materials;

- support and development of the industry talents.

In the summer of 2022, the US company Baker Hughes stopped servicing all Russian LNG projects and stopped its supply of equipment, including gas turbines (three out of seven LM9000 turbines intended for the construction of the first train of Arctic LNG 2).

Today, no more than 5% of Russian LNG production relies on domestic technologies. At the same time, Russian equipment is still unstable in operation, while Western equipment is no longer supplied due to sanctions, which forces companies to look for suitable solutions on the Chinese market.

At the moment, equipment has been delivered only for the Arctic LNG 2 project with a production capacity of 6.6 mtpa (9 billion cubic meters), while the implementation of other NOVATEK’s projects has been postponed indefinitely. In addition, the Syradasai coal project was halted in early 2023 due to problems with the supply of US equipment.

As far as LNG projects are concerned, they were mostly suspended after sanctions were imposed and European and American licensors pulled out. Besides, the domestic Arctic Cascade Modified gas liquefaction technology intended for large-scale LNG production has only recently been patented and the infrastructure for its implementation is not ready yet. Thus, the transition to the use of large-capacity domestic gas liquefaction technology is yet to be completed.

However, the first developments and prototypes, as well as cases of their successful commercialization have emerged across many priority areas outlined in Russia’s long-term LNG development program approved in 2021. This confirms the importance of expanding domestic R&D for high-tech equipment and transition to commercial operation.

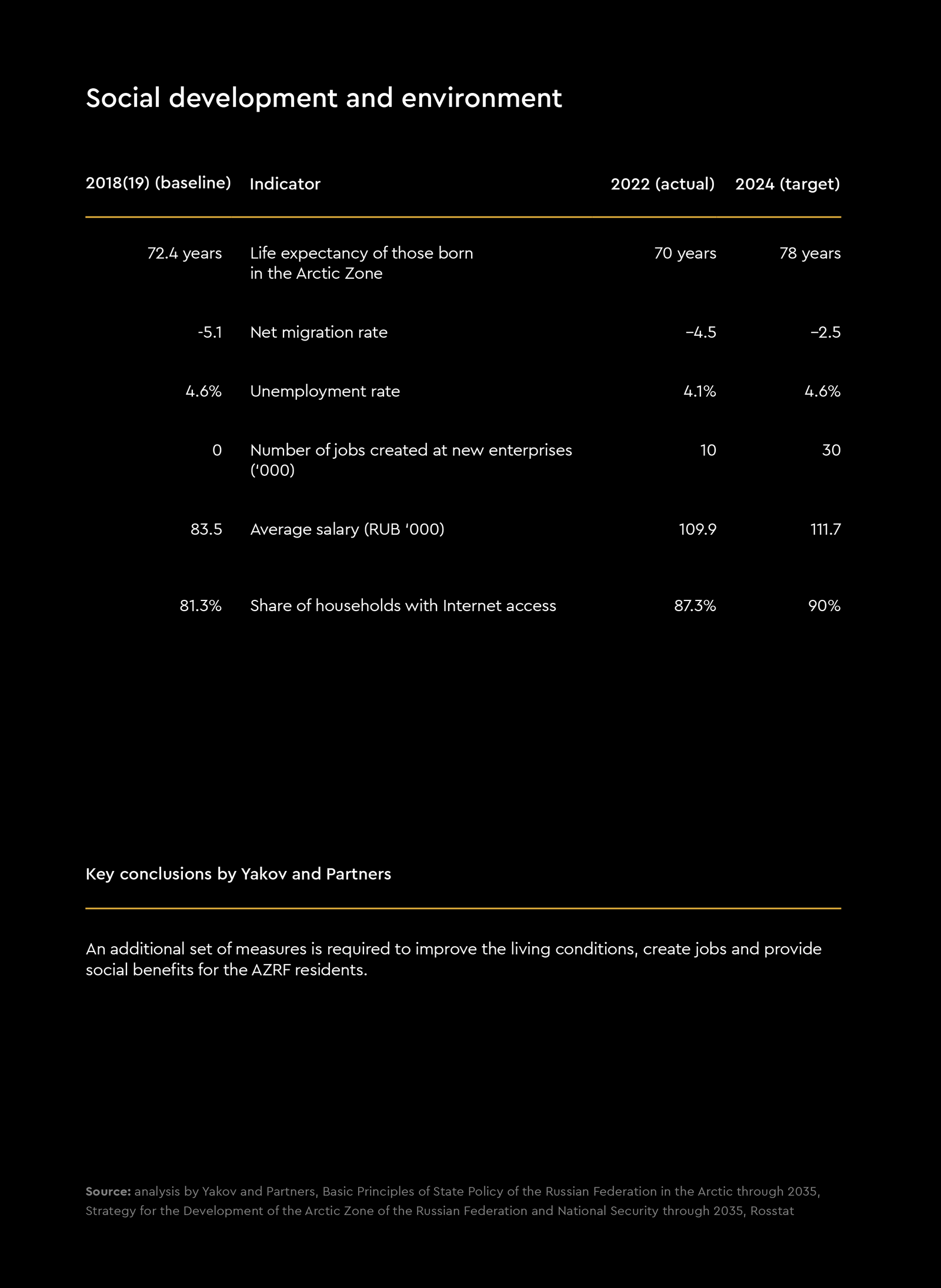

This year will mark the completion of the first stage of the AZRF Development Strategy, which means preliminary conclusions regarding the implementation status may be drawn. It will also be necessary to take action on indicators that will fall short of the targets.

As the long-term AZRF development strategy implementation progresses and nears the end of its first stage this year, it is necessary to analyze both early deliverables and obstacles to its successful implementation. The bottlenecks in the strategy, which was adopted in 2020 and does not take into account the new geopolitical realities, including sanctions risks, need to be thoroughly analyzed. This will facilitate the search for the most effective solutions when the strategy gets updated in the future. But it is already obvious that due to the "rightward shift" of many Arctic projects, the NSR cargo traffic targets laid out until 2035 will have to be revised, while some of the program indicators may fall short of the targets without additional support measures. We suggest the following (not exhaustive) list of updates:

- In terms of social development, we believe it is advisable to introduce additional measures aimed at improving the quality of life of the AZRF residents, since, unlike other regions and contrary to the goals of the program, life expectancy has decreased over the four-year period.

- It makes sense to increase the share of investment in the eastern part of the AZRF (the Far East), which, compared to the western part, has less developed transportation and energy infrastructure, yet is better positioned to accelerate Russia's "Turn to the East".

- It is crucial to multiply the level of funding and support for R&D projects related to developing domestic technologies and equipment for LNG production, shipbuilding, and small aircraft.

- In terms of resource and technological sovereignty, in our opinion, in addition to hydrocarbons, it is necessary to expand the strategy to include a list of targets on production of scarce minerals, whose potential is yet to be fully realized. First of all, these include lithium, manganese, and REM required for high-tech industries, chemical, and heavy industry.

The sanctions against the Arctic projects put an unprecedented pressure on all the stakeholders. The key risks include the lack of reliable sales markets for hydrocarbons, insufficient Arctic-class fleet to ensure reliable transportation along the NSR, and the lack of domestic equipment and technologies required to proceed with LNG and Arctic coal projects.

In order to preserve the sovereignty and ensure long-term sustainability of Russia’s Arctic territories amid intense global competition, Russia needs to continue consistent implementation of its comprehensive Arctic development strategy, which contemplates massive investments amounting to almost USD 190 billion. Yet given the increasing interest in the region shown by unfriendly countries, as well as the growing impact of friendly states in terms of sales markets and equipment, Russia needs to be prepared to further ramp up its investment despite already surpassing all other countries in terms of investment intended for the Arctic development. This will be driven, among other things, by increasing spending on Arctic projects. At the same time, a detailed analysis of the actual deliverables of the first stage of the Arctic strategy is needed to adjust further plans and possibly to add scarce minerals to the list. Key target indicators for the formation and development of mineral resource bases in the Arctic should obviously take into account not just the volume of mining, transportation, and export of those minerals, but also their contribution to the next process areas, as well as construction of facilities for advanced processing of concentrates of rare and rare-earth metals to produce pure metals and/or high-tech compounds on the basis of domestic technologies.

It is critical to consider the possibility of advanced development of domestic shipbuilding, especially Arctic-class transport fleet, to ensure cargo transportation along the NSR. Additional effort is required to develop and introduce domestic technologies and equipment for natural gas liquefaction and coal mining to reduce dependence on imported technologies.

In parallel, it is necessary to foster cooperation with friendly states, including China, to implement joint projects in the Arctic. This will help attract the necessary resources and expertise, as well as strengthen international ties and develop optimal routes to new markets for domestic products.

Taken together, the above measures will facilitate Russia’s adaptation to external change and help remove some of the main roadblocks in the way of successful development of Arctic resources and the use of the NSR, as well as help reinforce Russia’s dominance in this strategically important region.