Report

Is It Always Good to Be Open?

October 2023

Is It Always Good to Be Open?

In the next two years, the annual economic impact from open finance technology will be up to 300 billion rubles. Financial companies that can implement commercially successful business models based on open data will benefit the most.

The prerequisites are sovereignty and data openness – a combination that simultaneously ensures the stability and development of national financial systems. While sovereign payment systems make countries more independent from external shocks, open data fosters competition, new product development, and customer empowerment.

Data is a key resource for financial systems and players in their competition for customers. In recent years, regulators in many countries, including Russia, have been actively implementing mechanisms aimed at reducing barriers to data collection. Russia has already achieved significant results in the public sector, including the public services portal (Gosuslugi) that enables identification of individuals in financial and telecommunication services, the government procurement portals (Goszakupki) that administer procurement processes for millions of contracts, and the Interdepartmental Electronic Interaction System, which has freed people from the burden of collecting documents in different agencies. Information which has been the “new oil” that provides advantages to a limited group of its owners (mostly major companies) is now transforming into “new water” for all market players.

Data is a key resource for financial systems and players in their competition for customers

Digitalization of the Russian financial sector leads to fundamental changes in business models and emergence of new user scenarios. Following the implementation of digital financial assets and launch of the digital ruble, open finance technology will be the next major innovation. It provides for a phased implementation of open API standards in the banking, investment, insurance and microfinance markets in Russia in 2024–2025.

Yakov & Partners Finance Practice has analyzed global experience and stages of open data implementation, as well as the potential, specifics, and implementation scenarios for this concept in Russia. In addition to that, the research assesses the economic impact from introduction of open finance technology and subsequent transition to open data on the Russian market and all its players, i.e. the government, financial institutions, and customers.

Historically, financial institutions have been at the forefront of digitalization both in Russia and abroad, as their core business is based on big data. Moreover, banks have two other digitalization processes running in parallel. First, it is the bank’s internal digitalization, which includes managing customer experience and processes, and second, it is digitalization of communications with other financial institutions.

Thus, banks are the central element of the step-by-step opening of data

Thus, banks are the central element of the step-by-step opening of data. That provided, development and implementation of open finance in all countries are initiated by regulatory authorities: they are interested in improving the transparency of data and its sharing at the level of the entire market, as it stimulates competition for customers and improvements in the number and quality of services.

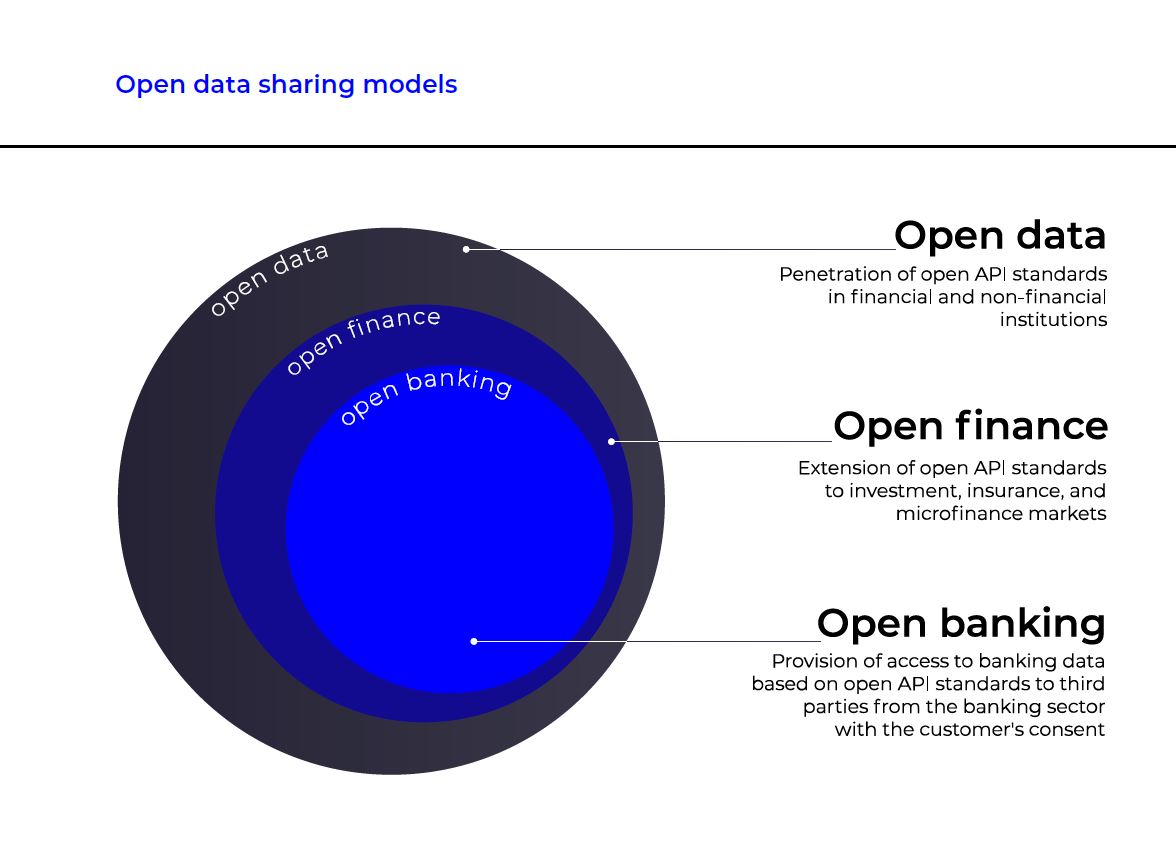

Digitalization of both the data itself and operations with it required standardization of information sharing. One of the results of that standardization was the open API technology. It enabled three open data sharing models both in the financial sector and beyond: open banking, open finance, and open data. All of them make it possible to collect information about customers with their consent, but they differ in the range of parties who have access to such data.

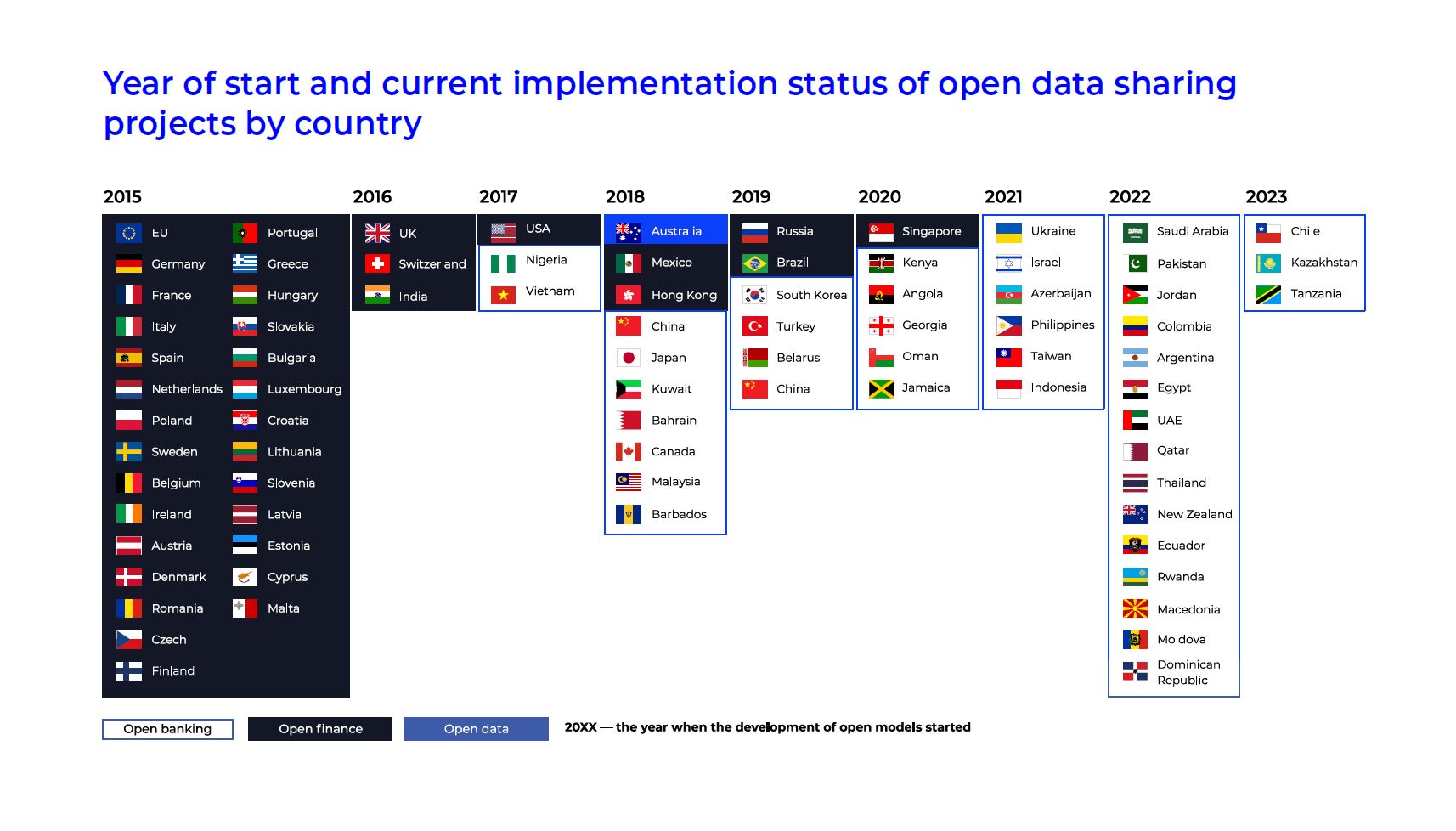

Implementation of open models globally started in 2015, when the European Union ratified the second Payment Services Directive (PSD2) requiring banks to provide data on customers’ accounts and debit monies from such accounts upon relevant request. In 2015, the first 27 member states of the EU joined the open banking model. Today, open models are implemented in more than 80 countries (out of nearly 200 worldwide) accounting for over 90% of the global GDP.

In the vast majority of cases, countries start implementing open models with open banking and, as they advance, they move on to open finance. Apart from the EU member states, countries that are currently at the stage of transition to open finance include the United Kingdom, Switzerland, India, USA, Mexico, Hong Kong, Brazil, and Singapore. The only country in the world that is already advancing to the third stage, open data, is Australia. In 2018, it extended its data sharing framework to the energy and telecommunications companies.

Based on the analysis of global practices, it is possible to identify three maturity levels for open data sharing models:

- Successful piloting and scaling of projects with subsequent advancement to new development stages (UK, Brazil, Australia, EU)

- Proactive introduction of open banking and/or open finance models and their first implementation (Russia, Mexico, Hong Kong, Singapore, USA)

- Exploring opportunities to implement open data sharing models (Argentina, Peru, Morocco, Niger, and other countries)

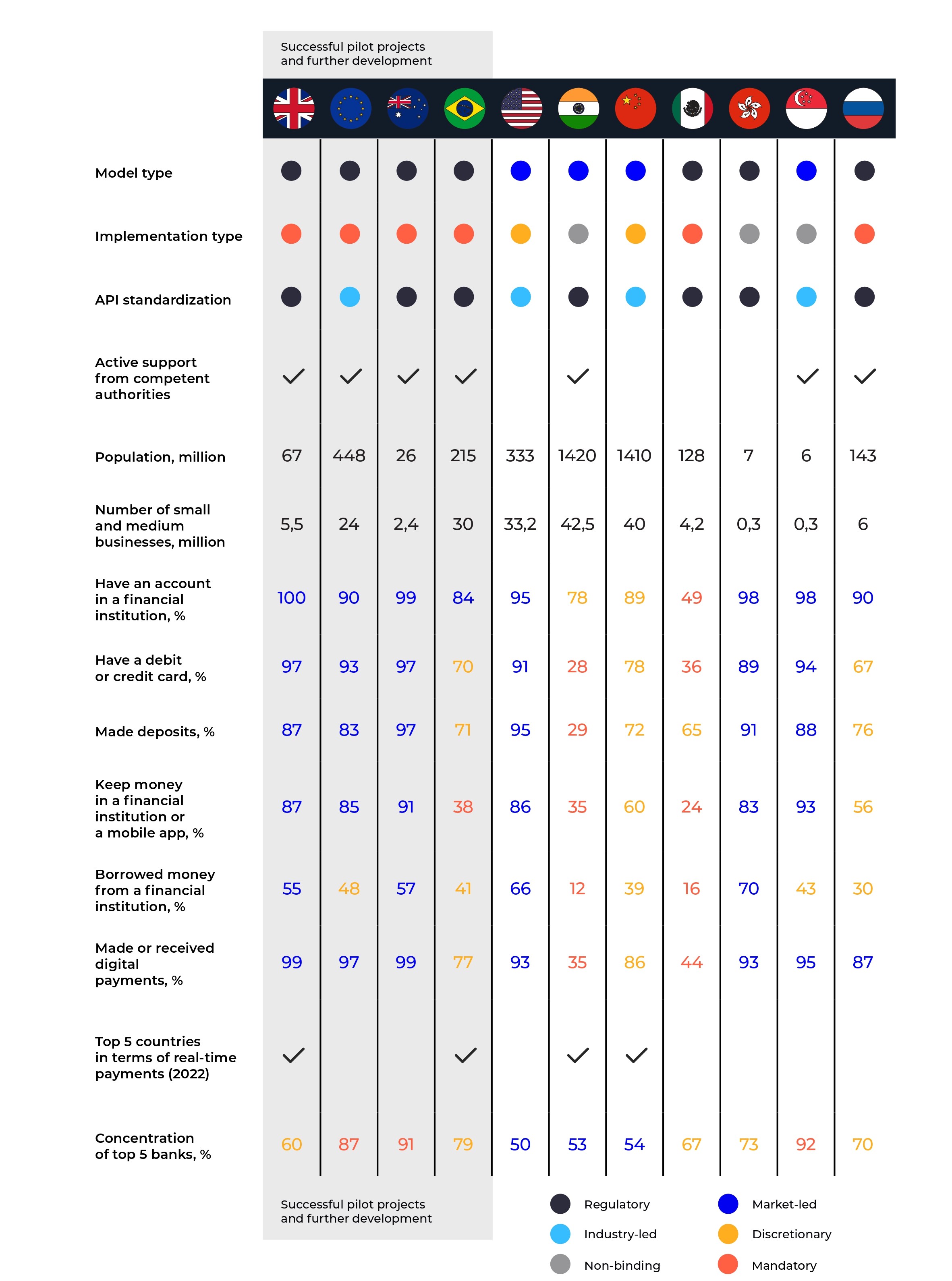

The United Kingdom is one of the European leaders in open finance development with tangible results. Having started in 2016 with the establishment of a dedicated entity responsible for open banking implementation (Open Banking Implementation Entity, OBIE),¹ the UK launched the first projects as early as in 2018. Two years later, the number of open banking users in the country reached the one-million mark. In mid-2023,² the number of monthly users was 7.19 million, which is more than 10% of the UK’s population. Total number of open API calls exceeds one billion a month (including almost 10 million payment requests) with the average response time of 0.4 seconds and the overall system availability rate of 99.8%. According to the 2019 estimates, the total economic impact from implementation of open models in the UK was 18 billion pounds.³ This included 12 billion pounds through the advancement of personalized customer products and 6 billion pounds through implementation of innovative management tools for small and medium businesses (SMEs). Based on these achievements, British authorities and financial institutions went on to develop plans for advancement to the second level model: implementation of data sharing for savings accounts, investments, loans, pensions, mortgage loans, and insurance, as well as for scaling the number of government services that are part of the data sharing framework.

18 billion pounds per annum – the overall economic impact of implementing open models in the UK

Apart from Australia, as mentioned above, the countries that have successfully passed the scaling stage include the EU countries and Brazil. In the beginning of 2023, most EU countries had at least 100 data sharing service providers, while the number of connected accounts in Brazil reached the five-million mark in just two years, which is five times faster than the UK or Australia.

What are the common features of successful global cases? They are standardization and regulation of processes, control and active involvement on the part of the government, and mandatory application of the models. The United States and China are the exceptions here, as these two countries opted for discretionary adoption of open data sharing models at the level of regions, industries or specific companies.

A mature national banking system is a prerequisite for successful development

Another important factor of success is the existence of a highly developed national banking system. However, there are examples to the contrary. In India, which is now the global leader in terms of realtime payment transactions, the underdeveloped banking system created a strong potential that stimulated the emergence of financial products eliminating the access gap. In addition to that, despite the non-binding nature of implementation, Indian authorities invested a lot of effort in establishing the open banking infrastructure. The size of the population and the scale of business activities in the country was yet another factor driving the economic impact from implementation. However, the lack of these advantages does not hinder the success of small, rapidly developing countries. For example, in 2018–2020, Singapore, a city-state with a population of about 6 million people, successfully advanced to the open finance stage thanks to high industry competition and mature financial sector.

Despite the fact that the regulator published the official concept of open finance development only in 2022, the project started much earlier – in 2016, when the Bank of Russia established the Financial Technology Department.⁴ That same year, the regulator and the largest market players set up the FinTech Association (FTA).⁵ Four years later, the first standards for open banking interfaces were published, and an open API environment was created on the FTA platform, which enabled its members to exchange financial information and run compliance tests on a certification stand. Thus, by 2022, the infrastructure for implementation of a particular open data model in the country was generally in place.

The Bank of Russia defended the choice of the open finance model (rather than the open data model) by arguing that it would help achieve economic “quick wins”, while implementing open data would require solving a number of cross-sectoral and regulatory issues that were beyond the scope of the regulator’s powers.

At the same time, “skipping” the open banking stage is reasonable for Russia for two reasons:

- First, the total assets of the Russian banking system in 2023 may exceed 150 trillion rubles, which is about 30 times as much as the assets of all insurance companies in the country (“only” 4.6 trillion rubles).

- Second, thanks to their technological advancement, banks can play the role of innovation leaders. Despite the elevated costs of technology upgrades, implementation of open finance can be expected to make a greater economic impact.

The Russian regulator has envisaged a phased strategy to implement the second-level model. In 2023, information about banks (addresses and opening hours of their branches and ATMs) will become available in mapping services on a non-binding basis. More detailed and valuable data will become available in 2024–2025. In 2025–2026, sharing of information about an entity, its products, and the products/ contracts of its clients will be mandatory for all financial market players (except for microfinance institutions). In the banking industry, payment initiation data will also become transparent. However, that transparency requirement will not apply to information about customers’ actions with their accounts or products.

The scope of open technology and its rate of development in Russia are in line with global best practices and project success criteria

All in all, the scope of open technology and its rate of development in Russia are in line with global best practices and project success criteria. The country has laid the foundation for advancement to open data: management and control bodies are in place, processes are regulated by law, and standards, regulations, composition of participants, scope of work, and requirements to infrastructure, including those to information protection, have been defined. Also, a list of products for open sharing has been developed, and a roadmap and schedules of pilot projects have been defined for phased and mandatory implementation.

The open finance model can become a new driver of growth for the Russian financial system. Over the previous 10 years, it has achieved impressive results in areas that provide synergies with open models for the national economy:

- In 2015, the National Payment Card System (NPCS) and the Mir payment system were established. It allowed to transfer the processing of domestic transactions with Visa and Mastercard cards issued by international payment systems to the NPCS.

- In 2019, the Faster Payments System (SBP) was launched. In 2020, Sberbank, which had previously dominated the payment market, joined the SBP.⁶ In the first quarter of 2023, 1.24 billion transactions totaling 5.38 trillion rubles were made through the SBP. One in two Russian citizens used SBP services for transfers, and one in four – for payments. Today, SBP meets nearly all the demand for payments from individuals. By comparison, the share of such payments in the UK is 42% of all API calls per month.

- The systems that enable transfers of funds between individuals (C2C), making payments for goods and services involving legal entities (C2B and B2C), and payments to the state (C2G) have been successfully implemented. Next in line is the system of payments between legal entities (B2B).

- The target availability rate for the operational and payment clearing center (OPCC) approved in the NSPC Strategy for 2023–2024 is at least 99.999%.⁷

Cancellation of charges for a significant portion of operations (first until June 30, 2022, and then until July 2024)⁸ served as an additional incentive for the implementation of open finance. Thus, Russia has already created a world-class payment system used by the financial industry to provide end users – individuals and legal entities – with a number of payment scenarios in order to simplify and accelerate their operations in the economy.

Of course, all this does not mean that the implementation of open finance is not associated with a number of risks.

1. Risks of personal data disclosure/loss and cybersecurity incidents.

In 2022 alone, the number of leaks involving personal data exceeded 600 million records,⁹ while information about nearly 100 million people was subjected to unauthorized access.¹⁰ New information security standards, more stringent controls, enhanced response measures, and tougher penalties are needed to mitigate these risks.

2. Risks of fraud by service providers.

To mitigate these risks, it is necessary to enhance verification and control measures and impose harsher penalties for providers. Although the number of transactions made without clients’ consent in 2022 decreased by 15.3% against the previous year, the total amount of banking transactions increased by 4.6%. The primary channels for fraud are online and remote services.

3. Risks of the customers’ lack of knowledge of / lack of trust in the system or their refusal to provide data.

Even countries that have successfully implemented pilot projects reported that 40–55% of people did not know about open banking. It is important to develop and implement an effective customer communication system, while taking additional measures to ensure protection of users.

4. Risks of further improvement of larger companies’ positions due to their gaining access to information about clients of smaller companies.

Additional supervisory and regulatory measures aimed at promoting competition are required to curb these risks.

5. Risks of the market players’ failure to meet open API infrastructure requirements or not being ready for such operations.

These risks can be mitigated through the development of standards and measures to support and adapt the parties to the data sharing process.

The new open finance model will benefit banks, which will pool their lending and transaction scoring competencies based on open APIs.

Implementation of the open finance framework in Russia will have an impact on three groups of beneficiaries. What will it bring to them?

Improved customer experience, increased loan availability, personalized offers, higher quality of financial services, and cheaper insurance and brokerage services.

Improved competitiveness for small and medium-sized financial market players and fintech companies, larger borrower base driven by access to transaction scoring data, cost-cutting potential for new integrations.

Improved competition and lower monopolization risks, broader access to finance and higher financial literacy of people.

The sources of benefits offered by open finance to users and financial organizations are four basic processes that serve as a foundation for growth scenarios. These are third-party access to customer information, data consolidation, savings management, and finance management.

Customers can get plenty of good opportunities by disclosing their personal information. For example, they can diversify their banks to receive an income at one bank, keep their savings at another, opt for a third one for their everyday spending, and arrange insurance at different insurance companies. Sending in queries about customers, all their accounts and contracts through open APIs makes certificates of earnings unnecessary. Rather than using a number of applications offered by different banks, customers get a one-stop financial app accumulating all their contracts, accounts and transactions, thus gaining integrated control over their finances across the entire range of loans, cards, insurance policies, and investments. By getting access to information on all the offers available from all the banks in the market, customers will be able to choose the best deposit deals, and transferring money from one bank to another will become a routine thanks to zero fees and instant execution via SBP.

Rather than using a number of applications offered by different banks, customers get a one-stop financial app

Customers will no longer have idle funds in their accounts, but get passive income, creating micro pools or splitting them up to get the best deal possible. The ability to browse the Internet to choose between different offers transforms the financial market into a global marketplace, enabling customers to find optimal solutions to each of their needs. For example, when arranging an insurance contract or looking for brokerage services in the investment market, customers will gain access to alternatives at better prices.

Open finance is no less beneficial for credit institutions. After disclosing data on their transactions, banks can improve their sales funnel by providing personalized, up-to-date offers – for instance, by increasing a customer’s credit card limit a month before their insurance contract expires. Since personal finance management can be implemented by small banks, fintech companies and ecosystem applications provided by marketplaces or telecoms alike, its market entry can create synergies thanks to stronger competition, increased customer attention and more frequent interaction. Pooling customer money from different sources can help increase the average ticket and improve the unit economics of services. Moreover, customers comparing different offers before buying products help improve nonprice competition between market players (more advanced product management options, service quality, etc.).

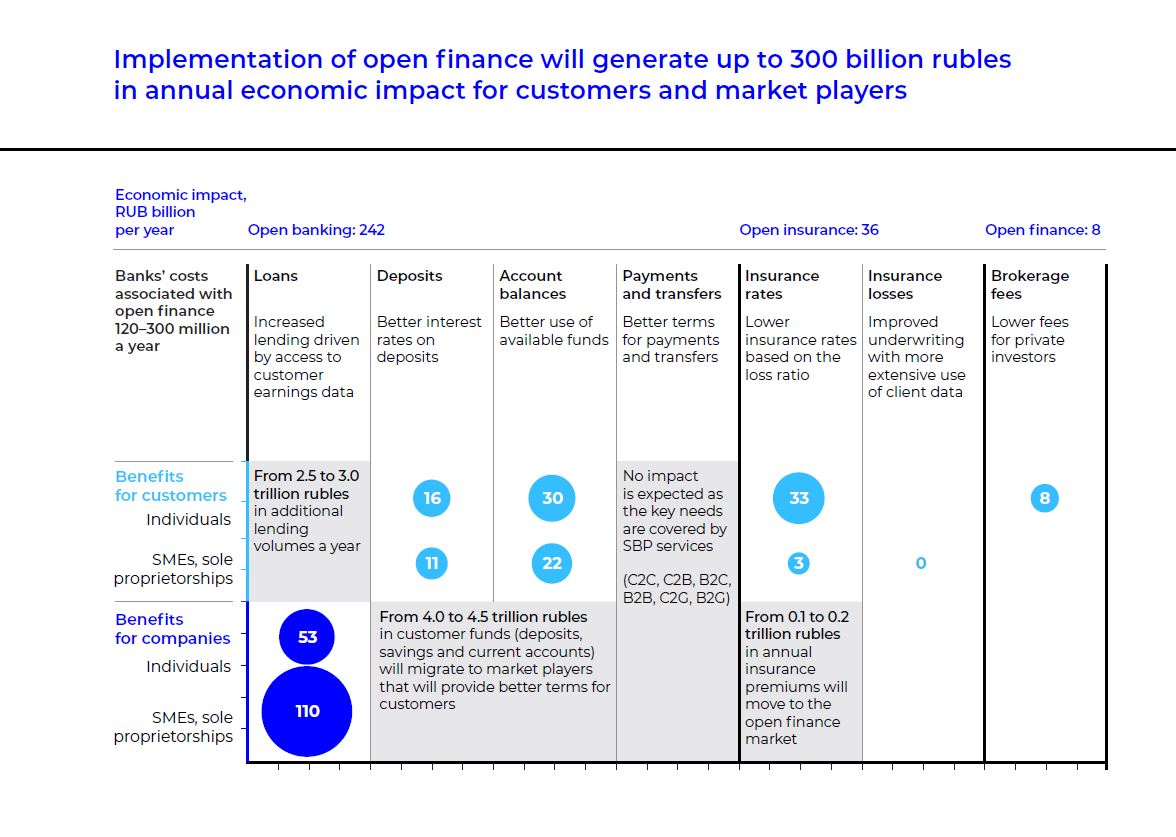

The cumulative impact of open finance – brought about by these scenarios only – will be about 300 billion rubles as early as in 2025. The introduction of open finance will not only make a tangible contribution to the profit generated by the banking industry but also provide a fresh impetus to the evolution of the Russian financial sector.

Open finance will provide a fresh impetus to the evolution of the Russian financial sector

It is worth mentioning that the bulk of the market players’ revenues resulting from the new framework (163 billion rubles, or 57% of the total impact) will come from loans to SMEs and individuals. Growth in lending will be achieved through a 3–6% increase in loan approval rate as banks will get access to information on their potential borrowers by analyzing their accounts at other financial institutions. In other words, the major beneficiaries of open finance will be banks, which will be able to pool their lending and transaction scoring competencies based on open APIs by 2025. The remaining 80 billion rubles a year will be customers’ benefits from using open finance technology to manage personal finances. These benefits will mostly come from the effective allocation of funds by using the most lucrative investment options and a 4–6% increase in the number of remote banking customers. This will inevitably lead to a redistribution of customer funds between market players.

Implementation of the open finance framework in Russia will take about a year. Most of the costs in three key areas – digital, operations and security – will come from teams and infrastructure upgrades. The key tasks are debugging and integrating bank systems and processes that record transactions requiring disclosure through APIs. These are client data storage and processing modules, account management and logging, contracts, front-end systems (mobile apps and online banking), and security and communications protocols.

Costs to implement open finance will range from 100 to 300 million rubles depending on the size of business and its technological maturity. They can be reduced by engaging the Bank of Russia and the FinTech Association¹¹ in standardization, piloting and expert support. Still, the banks’ implementation costs will be no less than 7–10% of their overall IT expenses.

While the implementation of open finance will bring customers and market players economic benefit of up to 300 billion rubles in 2025, transition to open data involving highly developed industries such as commerce and telecom (which are characterized by rapid technology monetization and use of big data) is expected to result in a multifold increase in economic impact. According to studies based on international benchmarks, thanks to higher accessibility of client and industry data, replacement of foreign IT solutions, and innovations in databases, the transition will increase the impact of implementation for all sectors of the Russian economy up to 1 trillion rubles¹² within two years.

In view of the historical growth rates, the multifold increase is achievable through joint actions taken by businesses and the government, use of data in civil law transactions, development of data sharing, and implementation of Russian cloud technology and platforms. Also, this will encourage banks to create premium APIs that provide third parties with access to wider data sets and enable banks to monetize services and build new business models on their basis.

The biggest impact from the transition to open data will be achieved in industries such as retail, finance, oil and gas, real estate and telecom, which will account for 70% of the total.

The biggest impact from the transition to open data will be achieved in industries such as retail, finance, oil and gas, real estate and telecom

Another incentive for the transition is data monetization, which can benefit a wide range of individuals and businesses, including customers as sources of data (individuals or legal entities) and companies that provide added value to the data (offering products to the customers). Customer data can be used for predictive analytics, platforms for acquiring banks, issuers and retail executives, platforms with insights for the retail sector, geoanalytics, improved online advertising for offline sales, etc. The overall market capacity may reach 316 billion rubles as early as in 2024.¹³

Even with the higher levels of data openness, the government will continue to perform the key regulatory functions. In addition to defining the basic standards and scenarios for open communication between different sectors of economy, the government can create growth opportunities for them through the use of solutions similar to Gosuslugi and the Goskey application.

After the National Payment Card System (NSPK), the Faster Payments System (SBP) and the digital ruble, the open finance framework is yet another element in the organic evolution of the Russian financial system. A number of banks have already started implementing open API standards, and the regulator is actively engaged in creating infrastructure needed to increase the number of players.

The open finance model provides banks with opportunities to boost their revenues by increasing lending volumes, with an estimated impact of about 163 billion rubles a year. Customers will also benefit from the open finance model, as they will get better investment opportunities, while the amount of additional investment can increase by up to 80 billion rubles a year.

The open finance model provides banks with opportunities to boost their revenues and customers will also benefit as they will get better investment opportunities

Despite the inevitable costs (up to 10% of the IT budget), financial institutions will also win from the new model as early as within a year, as they will be the fastest to provide access to data, pool their lending and transaction scoring competencies based on open APIs and adapt customer journeys in the key services.

Given the potential risks, including customer churn, banks will need to work hard to offer better financial terms and provide high-quality customer service beyond their products and services – it can also be provided based on open APIs. At the same time, financial institutions will have to continue optimizing costs and reducing the cost of funding to offer competitive prices.

Banks will also need to build up customer confidence to maximize the impact of open finance. In order to do this, financial institutions, together with the regulator, will have to create an effective customer communication system, while also taking measures to protect users and their data.

Successful implementation of the open finance framework in Russia will provide a sound foundation for the transition to the open data model, which has a potential economic impact of up to 1 trillion rubles within two years for a wide range of industries outside the financial sector.

1 Current name – OBL (Open Banking Limited).

2 Open Banking Limited, https://www.openbanking.org.uk/api-performance/

3 The Payment Systems Regulator Limited; The Financial Conduct Authority Limited; at the exchange rate of 123.91 rubles per 1 pound as of August 10, 2023.

4 https://www.interfax.ru/business/505512.

5 https://cbr.ru/press/event/?id=877.

6 The Bank of Russia, https://cbr.ru/analytics/nps/sbp/1_2023/.

7 NPCS, https://www.nspk.ru/upload/strategy-2324.pdf?ysclid=ll6dgu2w4a713438464.

8 The Bank of Russia, https://cbr.ru/PSystem/payment_system/2022-04-19_02/.

9 https://www.rbc.ru/technology_and_media/17/04/2023/643936229a7947134f0ce21c?ysclid=lms5sf9pzg695363510.

10 https://iz.ru/1459268/2023-01-24/obem-utechek-personalnykh-dannykh-rossiian-vyros-v-40-raz?ysclid=lms5yil48r631493804.

11 Big Data Association in collaboration with Digital Economy, an independent nonprofit organization, a report at First Russian Data Forum 2023.

12 McKinsey Global Institute, Financial data unbound: The value of open data for individuals and institutions, June 2021; Big Data Association in collaboration with Digital Economy, an independent nonprofit organization, a report at First Russian Data Forum 2023.

13 Big Data Association in collaboration with Digital Economy, an independent nonprofit organization, a report at First Russian Data Forum 2023.